Occupational and Final Salary Pension transfers to a Personal Pension Plan (PPP)

Occupational and Final Salary pensions, sometimes called Defined Benefit Schemes, are considered the gold standard of pensions. They provide the member with a guaranteed pension, usually linked to inflation, for life. The amount of pension will depend on the particular scheme benefits but are usually based on the number of years of employment and the final salary or career average salary of the member. In the event of the members’ death, their spouse will usually receive at least half the pension awarded to the member for the duration of their life. After the death of the spouse all payments will stop.

The value of the pension payments delivered by these schemes has always been near impossible to match in any defined contribution scheme, because the Final Salary schemes state at the beginning of the contract the benefit that will be paid regardless of prevailing market conditions, where as a defined contribution pension is left to market forces and the level of contributions to give a return.

Although many defined benefit schemes have greatly increased the member contributions required and are also moving to career average earnings instead of final salary, they often still represent the best possible pension provision.

However, there are certain advantages afforded to Personal Pension Plans (PPP) that make them highly attractive options for some final salary scheme members to consider transferring their defined contribution pension value into a PPP.

Why consider a transfer to a Personal Pension Plan (PPP)

Flexibility

Personal Pensions Plans (PPP) can be hugely flexible in how they deliver income. The holder can elect to take as much or as little as they like as income, depending on their tax status at the time. It is easy to see how advantageous this can be to some people who may have considerable additional wealth or who will continue to produce an income after the pension is payment.

Additionally, the Tax Free Cash element of the PPP, which is 25% of the total value, can be taken as one whole lump sum or as small amounts at any time after age 55, giving the pension holder great flexibility in how they manage their finances and taxation.

So for example, someone who was receiving a state pension of £10,000 and also had an income of £20,000, would end up paying tax at their marginal rate if they had a final salary pension income on top of that. This may mean they would be paying 40% on some income. As the final salary pension can not be reduced or deferred once in payment they would have no choice or control.

On the other hand, if that person had a PPP, they could take as little or as much income as they required at the time, therefore not paying any more tax than is required and retaining the value of their pension until it is required.

Guarantees

In the past, the only way to give a pension holder guaranteed income for life was either from a Defined Benefit scheme, or for a Personal Pension plan holder to purchase an annuity, both of which have limited or no death benefits, and no flexibility.

In the last 5 years there has been huge development in the retirement product market and there are now many different types of product that will guarantee an income for life regardless of investment performance. These are fully covered by the Financial Services Compensation Scheme (FSCS). Crucially, they also give full death benefits and considerable flexibility for taking income as required.

We should point out that as yet, there is no product that once in payment will also guarantee growth in line with inflation, as is the norm with a defined benefit pension.

Death Benefits

- Final Salary / Defined Benefit schemes.

Most final salary or defined benefit pension schemes have straight forward benefits for a surviving spouse, which usually amount to 50% 0r 60% of the full pension their partner was receiving prior to death. If death occurs before the scheme member has actually retired, there is usually an additional tax free death grant equal to 3 times the scheme member’s gross pay. In a few cases there may also be a smaller death grant lump sum payable even if the scheme member had retired and was in receipt of the pension for a relatively short time. However, assuming there are no children under the age of 18 (or in full time education), this is where the benefits stop. When the surviving spouse passes away, the pension ceases. If there is no spouse, or if the spouse passes away before the pension holder, there is no additional benefit paid.

- Personal Pension Plan (PPP)

A Personal Pension operates under a completely different set of death benefit rules which will change radically in April 2015 since the announcement by George Osborne in October 2014.

If death occurs pre age 75, the spouse, or whoever the pension owner wishes (children, grandchildren), may inherit the pension tax free to use as they please. This applies to both crystallised pots where tax free cash has already been taken, and uncrystallised pots which are “in-tact”.

If death occurs post age 75, the pensions may still be left to whoever the donor wishes. The crystallised pot is passed on tax free but must be used for income which is taxed at the new owner’s marginal rate. The uncrystallised pot can be taken as a lump sum, less a 45% tax. Therefore, forward financial planning is recommended well before age 75, to ensure little or no tax is paid.

Who should consider a transfer to a PPP?

Families where both spouses have a final salary pension:

These families are in a position to consider transferring one pension to a personal pension, with all the benefits that go with it, whilst retaining the benefits of the other final salary pension.

Families where their total income is considerably greater than required:

In these situations, especially where one spouse will carry on earning an income after the income from the final salary scheme starts, there is great advantage in having a control over how much income you actually take from the pension, especially if means staying out of the higher rate tax bands. As there is no control over income levels with the final salary scheme, it may make sense to consider a transfer to a PPP, where the amount of income taken is completely flexible.

Families or single people with additional wealth:

Where there is additional wealth, to the extent that some or all of the pension payments are not required on an on-going basis, there is little benefit in having a final salary plan and a transfer would make good sense.

Single people:

Sometimes a single person has final salary benefits in excess of their requirements and also does not require the spouses benefits given by a final salary plan.

Who should not consider a pension transfer?

Although proper in depth investigation is required to determine the true status of anyone considering a transfer, a rough guide would be anyone who thinks they require every penny, or anywhere close to every penny, that can be delivered as income from a final salary scheme. For example, if your total income requirements are £25,000 gross per year, and your total income including the pension is £30,000 per year, it is unlikely you should consider a transfer.

Personal Pension Structure and Strategy

Personal Money Management specialise in the design and implementation of pensions to fit each individuals client’s requirements and circumstances. Pensions can now hold a vast array of products and investments, each with their own profile and benefits. We work with the client to determine exactly which products, in which proportion, will deliver the best results for the client.

Crucially, the pension plan is now a dynamic instrument that can, and should be, altered over time to adjust to the clients age and priorities.

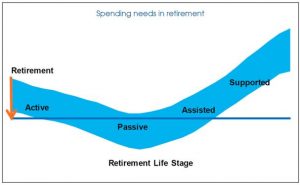

The diagram above shows how retirement is now a journey that can last as long as the working career. At the beginning the retiree is fit and active, which means they may well require more potential income to pay for their activities. As time goes on, they will do less but will want the security of guaranteed income to maintain a certain standard of living. As life progresses, they may have to consider issues such as assisted living, care home fees or the passing on of wealth if they have sufficient funds.

This diagram demonstrates the requirement for a dynamic pension and retirement strategy which can use different products at different stages to great effect. The days of a single product retirement vehicle for many have now gone.

Personal Money Management Pension Investment

Personal Money Management (PMM) only use mainstream FCA authorised and regulated investment products in their pension strategies. We do not make any direct investment in shares or bonds, although should the client wish this service we can appoint a Discretionary Fund Manager to do this for them.

• PMM is directly authorised by the FCA, firm no: 176616

• PMM never holds client money, all cheques are made payable direct to the product provider.

• PMM are fully covered by the Financial Services Compensation Scheme (FSCS)

• PMM are fully covered by Professional Indemnity Insurance.

Warning

At present, many members of final salary pension schemes are being contacted by unregulated and unauthorised pension “liberation” companies, who offer to transfer the benefits in a final salary scheme into a new plan, often overseas, where the client can gain access to the funds before age 55 or as a lump sum post age 55.

Any company offering such benfits is operating illegally. If you are in communication with any firm on these matters we recommend you contact the Financial Conduct Authority (FCA) immediately . You can find more information here: https://www.fca.org.uk/consumers/scams/common-scams/early-pension-release-liberation